The Involuted Biped: the Humanoid Race is Crowded and Wide Open

Inside the filings of the world’s densest robotics cluster: how China bootstrapped its humanoid demand, and where the “American brain” theory is cracking.

Humanoids are not about to replace labor, and the race to build them is, for now, almost entirely Chinese. We dive deep into the financial filings to discuss three things the headlines miss.

First, the rapidly involuted humanoid market in China means no winner has emerged. 90 new humanoid makers entered the market in the last 7 months of 2025. Unitree and AgiBot are neck-and-neck in total shipped units, and the tier-two players are scaling by multiples.

Second, China’s manufacturing lead is not just about cost, but also iteration speed. Vertical integration into its own actuators allowed BOM costs to fall by two-thirds in two years. It also allows robotics teams to iterate faster. Components get redesigned the same day in Shenzhen versus weeks across the Pacific.

Third, the “China brains” now top the open leaderboards. Closed US models don’t post to those benchmarks, so they sit unmeasured. The “China-body, American-brain” theory is being contested.

In addition, we discuss how Washington is already moving to keep the strongest Chinese maker out, protecting American and allied robot makers from China’s cost advantage.

The filings let us say all of this with numbers instead of vibes.

This report answers the following questions:

Who is actually shipping humanoids?

Who buys them, and for what?

How did China get here?

What does a humanoid cost now?

Who makes money today?

Can Unitree win the world, but still lose the US?

Is “China-body, American-brain” true?

What still stands between humanoids and real work?

Who is actually shipping humanoids?

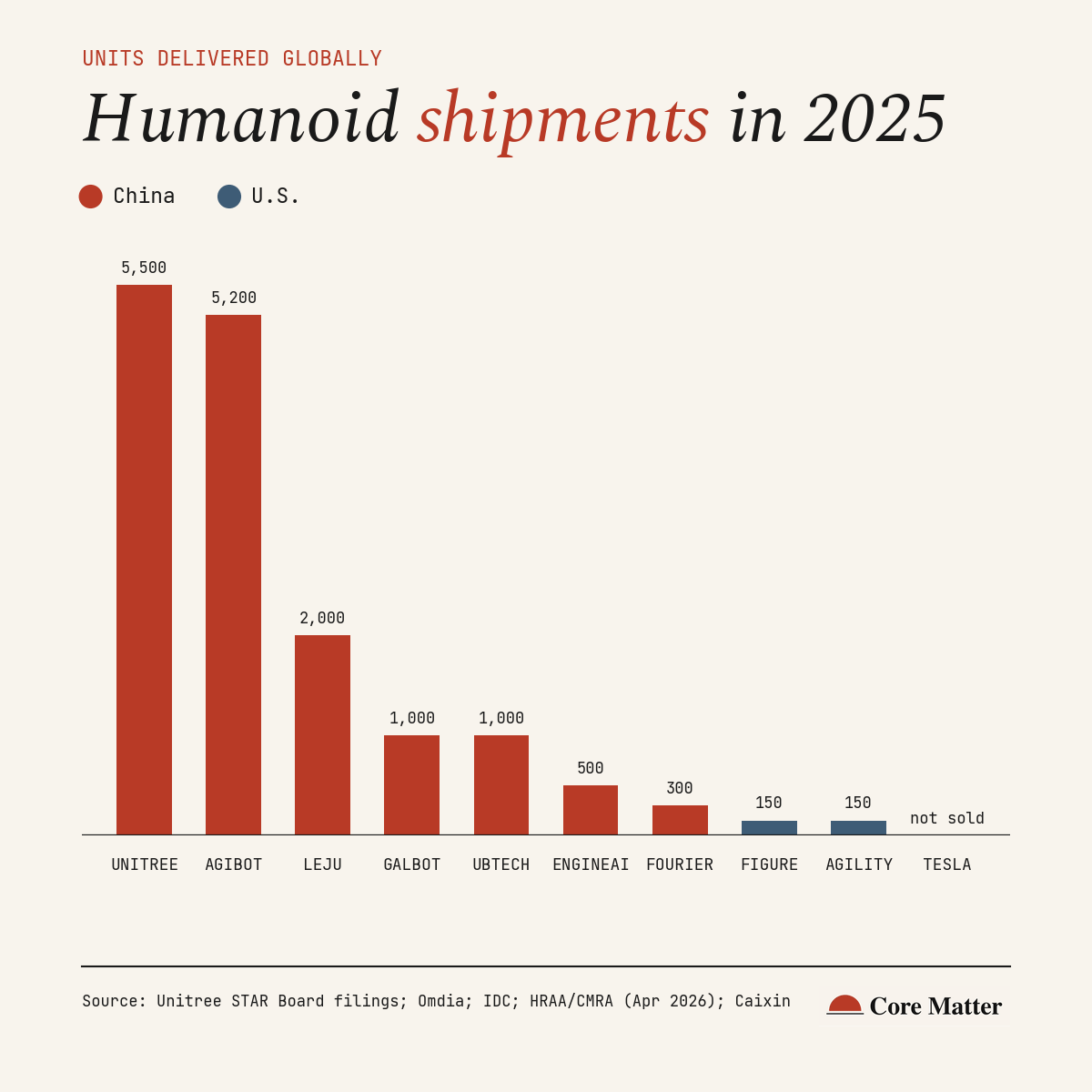

In 2025, Western trackers (Omdia, IDC) counted 13,000 to 18,000 humanoids shipped worldwide. Chinese industry body HRAA counted ~20,000 in China alone (Exhibit 1).

Unitree is the name everyone knows. It does lead the humanoid market by number of units shipped, but in a rapidly involuted market, the lead is narrower than its profile suggests.

Unitree shipped more than 5,500 humanoids in 2025, per its own STAR Board prospectus, a figure it defines as delivered to customers, not orders, excluding dual-arm wheeled robots, with production exceeding 6,500 units. Omdia’s January report had estimated Unitree at 4,200 units and ranked AgiBot #1; Unitree issued a public clarification on January 22 correcting the count upward by roughly a third, weeks before its listing-committee hearing.

AgiBot shipped 5,168 units per Omdia (5,200 per IDC), a count that includes its wheeled and half-size forms alongside full-size bipeds. On IDC’s full-size-only cut, AgiBot’s figure drops to ~1,300. Unitree maintains a definitive lead in pure-biped form factors, whereas the two firms achieve nearly the same aggregate volume.

Below them: UBTech at 600 to 1,000 units, and EngineAI and Robotera each above 500 units per HRAA.

In the US, for comparison, Figure and Agility Robotics shipped roughly 150 units each in 2025, from public reports cited in Unitree’s own inquiry response. Tesla’s Optimus does not sell externally. Tesla deploys it internally, which functions as a captive market.

Unitree, in other words, is the largest player in one of the most involuted markets in Chinese tech. China had more than 140 humanoid manufacturers offering 330+ models in 2025, per MIIT; registered manufacturers went from 110 in April to over 200 by November per CMRA and HRAA - roughly 90 new entrants in seven months, many well-funded and several founded by Huawei and BYD alumni. AgiBot claims the deployment lead outright, and is targeting a listing this year; Galbot is reportedly next; EngineAI confidentially filed on June 12 and disclosed its 2026 shipment target at 4000-5000, more than 10X its 2025 shipments.

“The industry is already seeing signs of involution, particularly in semi-humanoid robots and entertainment-oriented robots, where barriers are lower and prices are falling quickly,” said Yao Maoqing, a partner and senior vice president at AgiBot.

The competition is already showing up in prices: Unitree’s own filing attributes its 2025 price cuts to consolidating its position as the field crowds in.

Shipments are the best available scoreboard. Yet the winner is not decided, with Unitree and AgiBot almost tied. Other players are rapidly growing, with 90 more entrants. Where the robots got shipped and whether they are put to productive work is a separate question.

Who buys them, and for what?

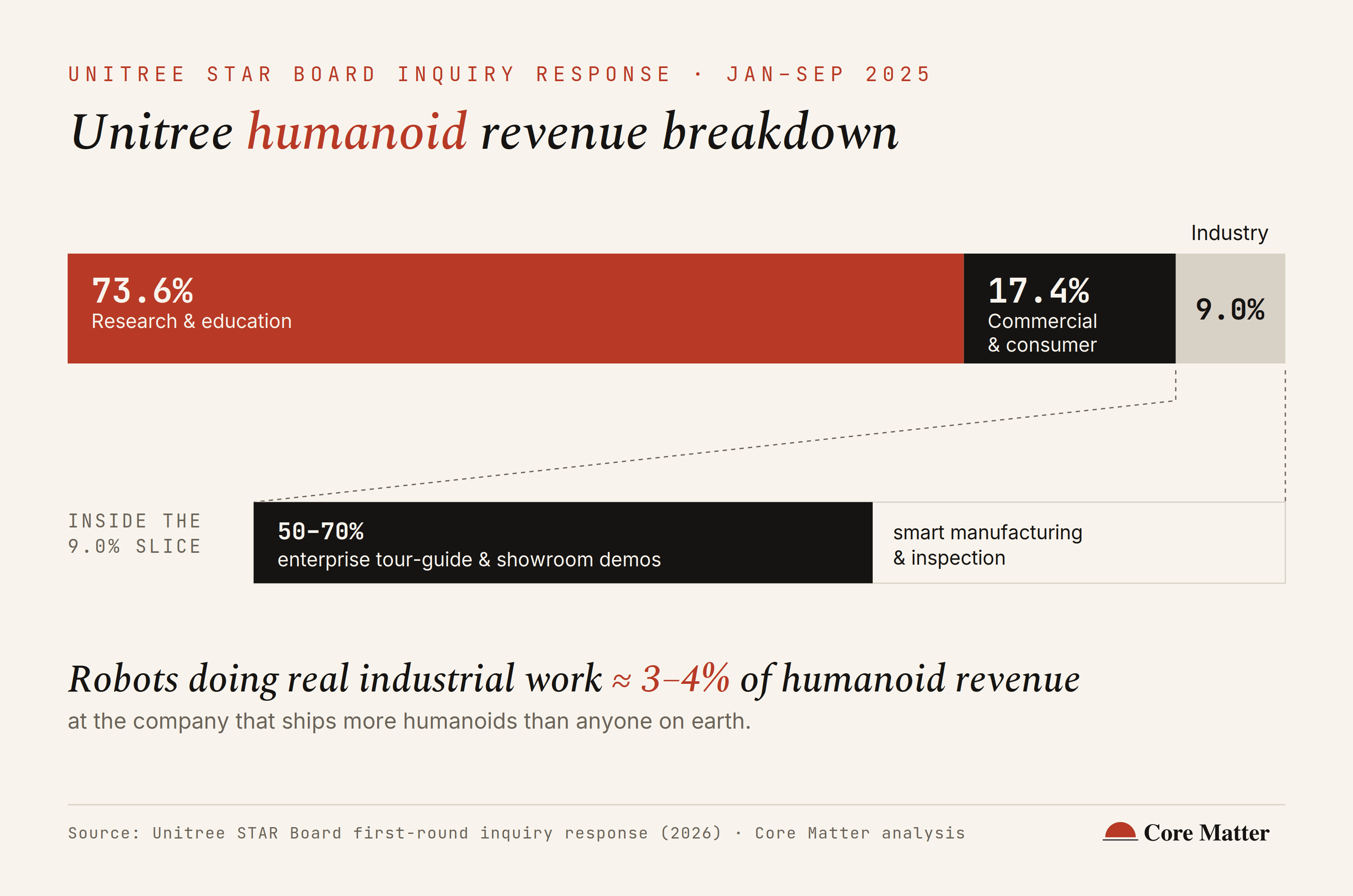

The STAR Board inquiry process required Unitree to break humanoid revenue down by application domain.

As Exhibit 2 shows, from January to September 2025, research and education represents 73.6% of Unitree’s humanoid revenue. Commercial and consumer, retail display, events, performances, science museums, 17.4%. Industry application, 9.0%.

Within that 9.0% industry slice, the largest use is enterprise tour-guide and showroom demonstration, at roughly 50 to 70%. Smart manufacturing and inspection make up the remainder.

Robots doing actual industrial work, carrying, assembling, inspecting, account for roughly 3 to 4% of humanoid revenue at Unitree, the company that ships more humanoids than anyone on earth. This is the 3% problem: the gap between what ships and what works.

The “deployed” humanoid in 2025 is mostly in research and academia. The “industrial” humanoid is giving office tours. Unitree says this itself, in regulatory language: research-domain demand is “more real and leading” (p.8, Unitree listing inquiry document) at this stage.

Is the demand real, or subsidy theater?

The customer data says it is real, with a structural qualifier. Unitree’s top five customers account for just 10.6% of revenue (max single customer: JD.com at 3.5%), related-party sales run under 1.5% of revenue, and overseas customers contributed 55 to 57% of revenue every year from 2022 through 2024. This is a diversified, arms-length, half-foreign revenue base. No concentration, no captive buyers, no round-tripping visible in the filings.

However, at the demand level rather than the customer level, a large share of the Chinese revenue is ultimately government money. The research segment is substantially state university and institute budgets.

On June 9, MIIT and SASAC jointly directed local governments and state-owned enterprises to deploy embodied AI across manufacturing, logistics, retail, and healthcare, targeting roughly 10,000 humanoids in commercial use by end-2026. State Grid, the largest SOE utility, is running a robot fleet procurement program against this mandate. Unitree’s prospectus itself attributes the 2025 domestic surge, which flipped its revenue mix from majority-overseas to 60.8% domestic in nine months, to the Spring Festival Gala appearance plus “domestic robotics policy tailwinds.”

Embodied intelligence now sits in the 15th Five-Year Plan. Being part of China’s economic planning document for 2026-2030 means having central funding priority, which cascades into provincial subsidy programs, SOE procurement mandates and university equipment budgets.

Education-sector demand is real but subsidy-shaped. Buyers are overwhelmingly public universities, vocational schools and institutes whose robot purchases draw on government education, research budgets, and provincial AI-education initiatives. The demand is driven by budget allocation, rather than commercial ROI.

The revenue mix is healthy, while the demand behind it is state-channeled. We discuss in the next section how that demand got built.

How did China get here?

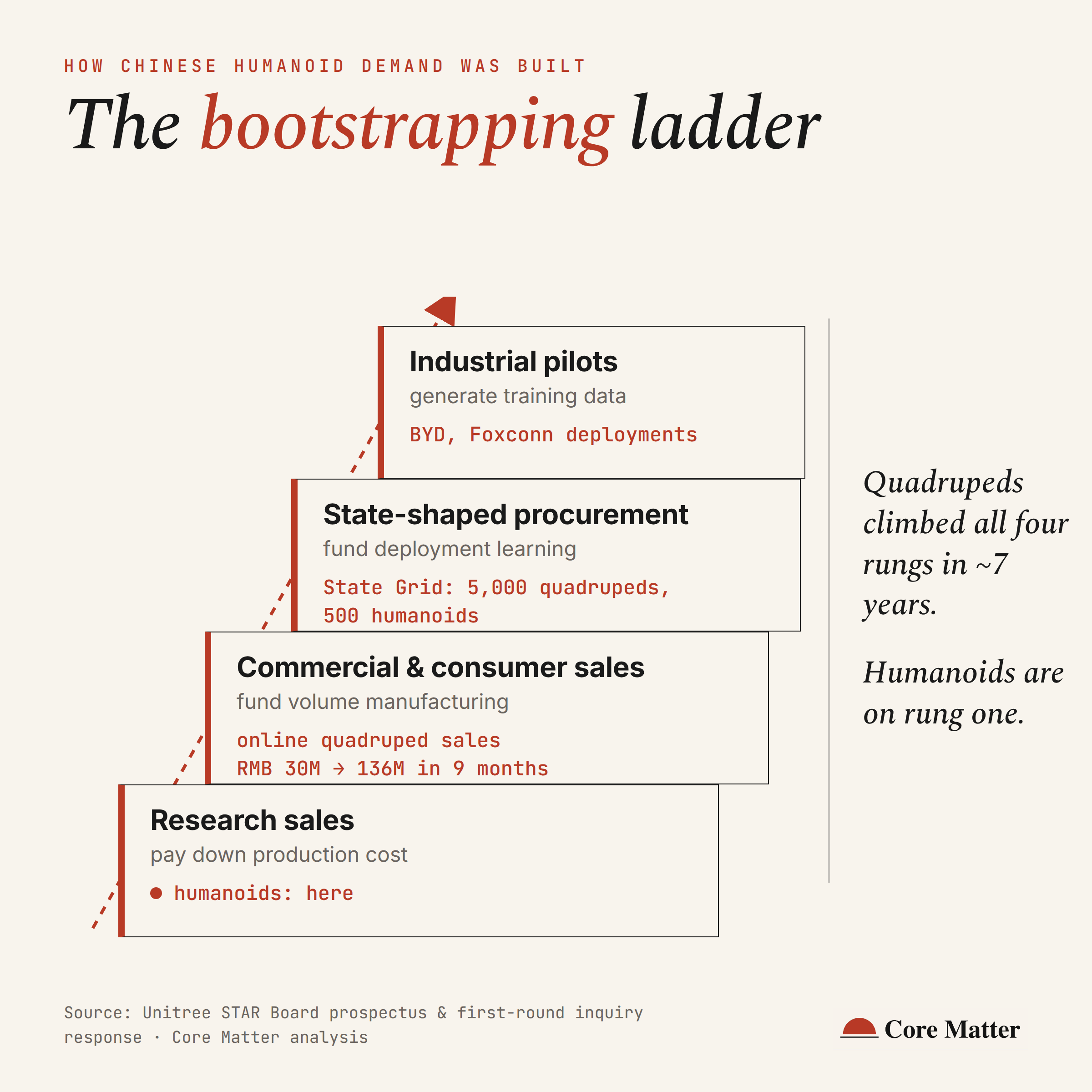

Demand: bootstrapped in four stages

The Chinese robotics market climbed a 4-rung ladder, each rung funding the next. Call it the Bootstrapping Ladder (Exhibit 3):

Research sales pay down production costs: every G1 sold to a lab at $16K pays down tooling and actuator iteration.

Commercial and consumer sales fund volume manufacturing: showrooms, events, online consumer purchases.

State-shaped procurement funds deployment learning: State Grid’s fleet plan alone calls for ~5,000 quadrupeds, 3,000 dual-arm wheeled robots, and 500 humanoids in substation and inspection roles.

Industrial pilots, the BYD and Foxconn deployments, generate the training data.

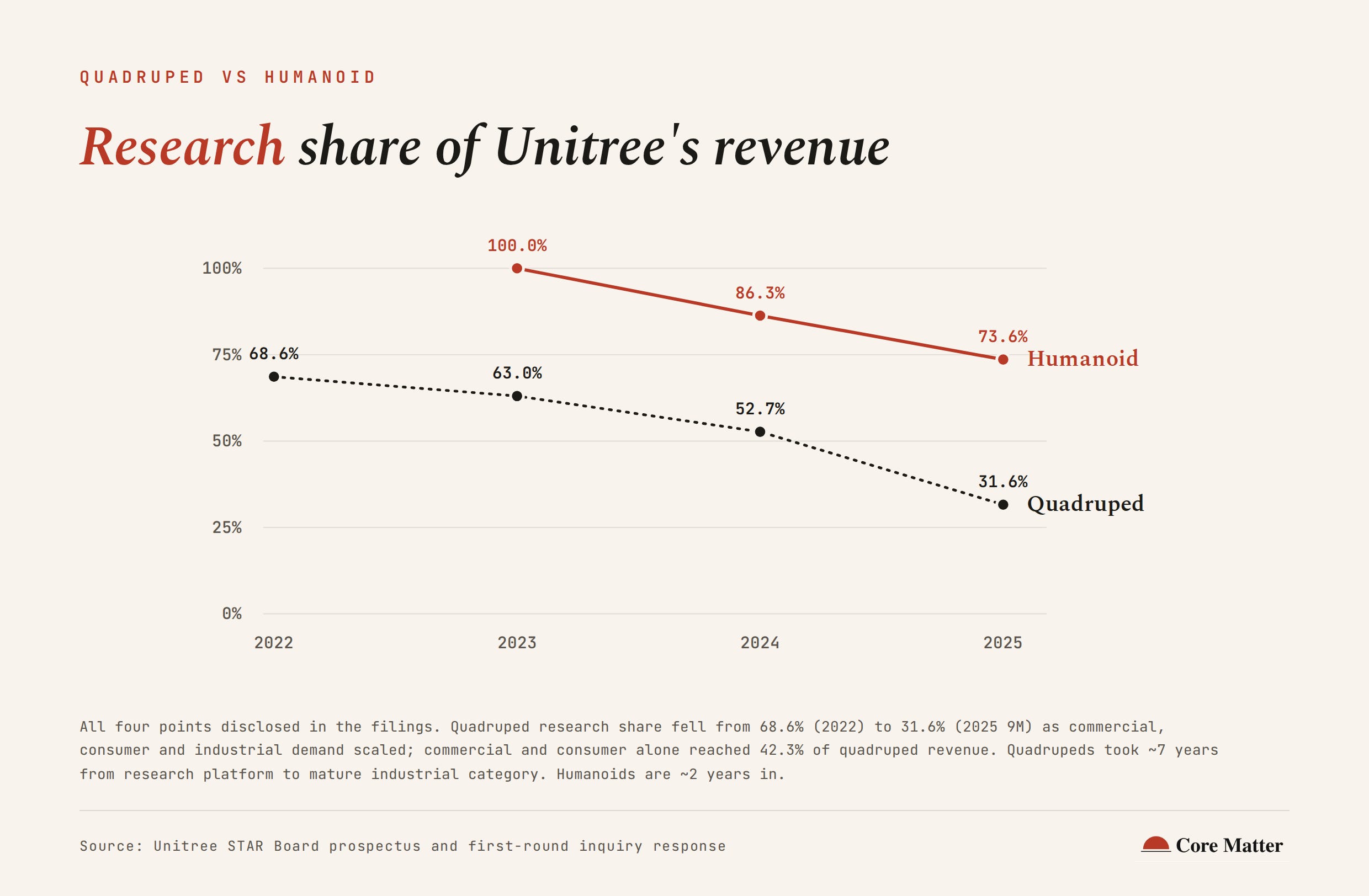

The quadruped business proves that the Bootstrapping Ladder works (Exhibit 4). In 2022, 68.6% of Unitree’s quadruped revenue was research. By January-September 2025, commercial and consumer had overtaken research at 42.3% of quadruped revenue, driven by online consumer sales rising from Rmb30mn in all of 2024 to Rmb136mn in nine months. Industrial quadruped work, power-station inspection, fire and emergency response, is now described in the filing as “relatively mature.” That climb took roughly seven years from research platform to mature industrial category. Humanoids, on the same company’s own domain-mix data, are at the start of that sequence, not the end.

US humanoid companies are running a different play: sell directly into the hardest rung, commercial labor or home chores replacement, with venture capital substituting for the missing intermediate revenue.

Figure and Apptronik run industrial pilots at Western cost structures with no research volume to pay down production costs. Agility sells logistics deployments at a ~$250K ASP against a compressing price curve. 1X is betting on a consumer rung that no company in either country has yet proven. Tesla’s program is captive and faces no external price discipline at all.

The two playbooks optimize for different things first: China for manufacturing scale, the US for software capability. A non-Chinese humanoid company has to win industrial customers directly, with no research volume and no state procurement underneath it.

Supply: own the price, own the pace

China did not invent the humanoid. It built the machine that makes them cheap, out of decades of manufacturing depth and deliberate vertical integration.

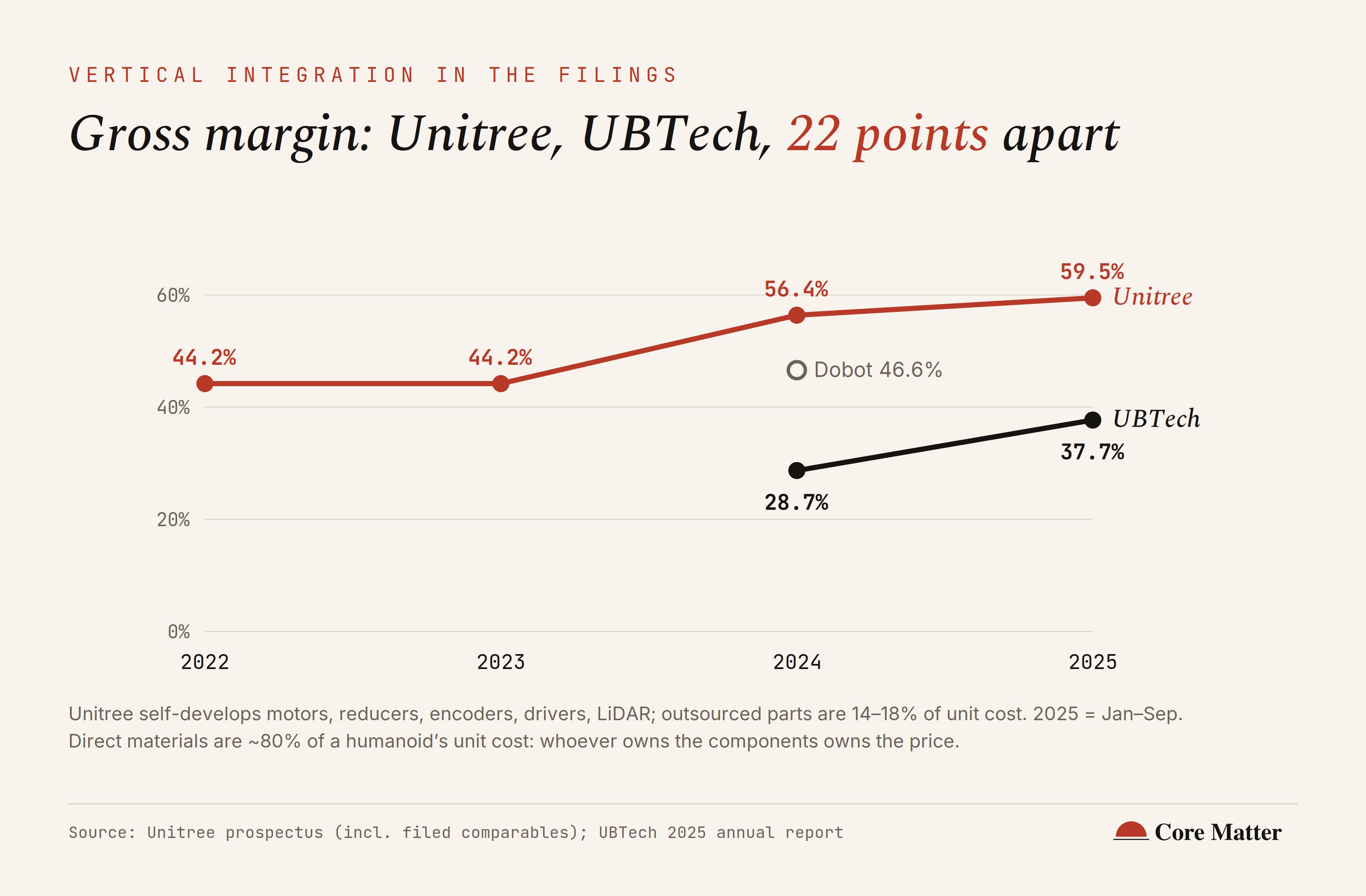

Unitree is one example of such deep vertical integration. Its filing describes the cost lead: “full-stack self-development” (”全栈自研”) of motor drives, mechanical structure, and control software. Motors, reducers, encoders, drivers, and LiDAR are designed and produced in-house; only battery cells, compute, and storage are bought in.

Outsourced components run just 14 to 18% of unit cost, excluding optional high-spec parts. Direct materials are roughly 80% of a humanoid’s unit cost. Whoever owns the components owns the price.

The margin record shows the integration compounding (Exhibit 5). Unitree’s gross margin climbed from 44% in 2022 and 2023 to 56.4% in 2024 and 59.5% in the first nine months of 2025, as in-house component volume scaled. UBTech, which assembles more than it makes, ran 37.7% in 2025, up from 28.7%, and Dobot 46.6% in 2024 per the comparables Unitree filed. A 22-point gross margin gap between the two public humanoid makers is the price of the difference between designing your own actuators and buying them.

The same southern China supply chain that makes components cheap also makes them fast. A new actuator design can be quoted, machined, and back in a robot’s hands the same day. The same process takes weeks when sourced from across the Pacific.

Even the US humanoid makers building ‘American’ robots are not insulated from this. Figure, Apptronik, and Agility all source motors, gearboxes, and electronics from the same Shenzhen-area supply base Unitree sits inside. They just do it from 7,000 miles away, on container-ship and air-freight timelines instead of same-day ones.

The same proximity that compresses hardware iteration also compresses the test-deploy-retrain loop for the embodied models in section 6.

The integration is replicable, but not quickly, and not at 150 units a year. It pays back through volume, and volume is what the demand-side ladder delivers.

What does a humanoid cost now?

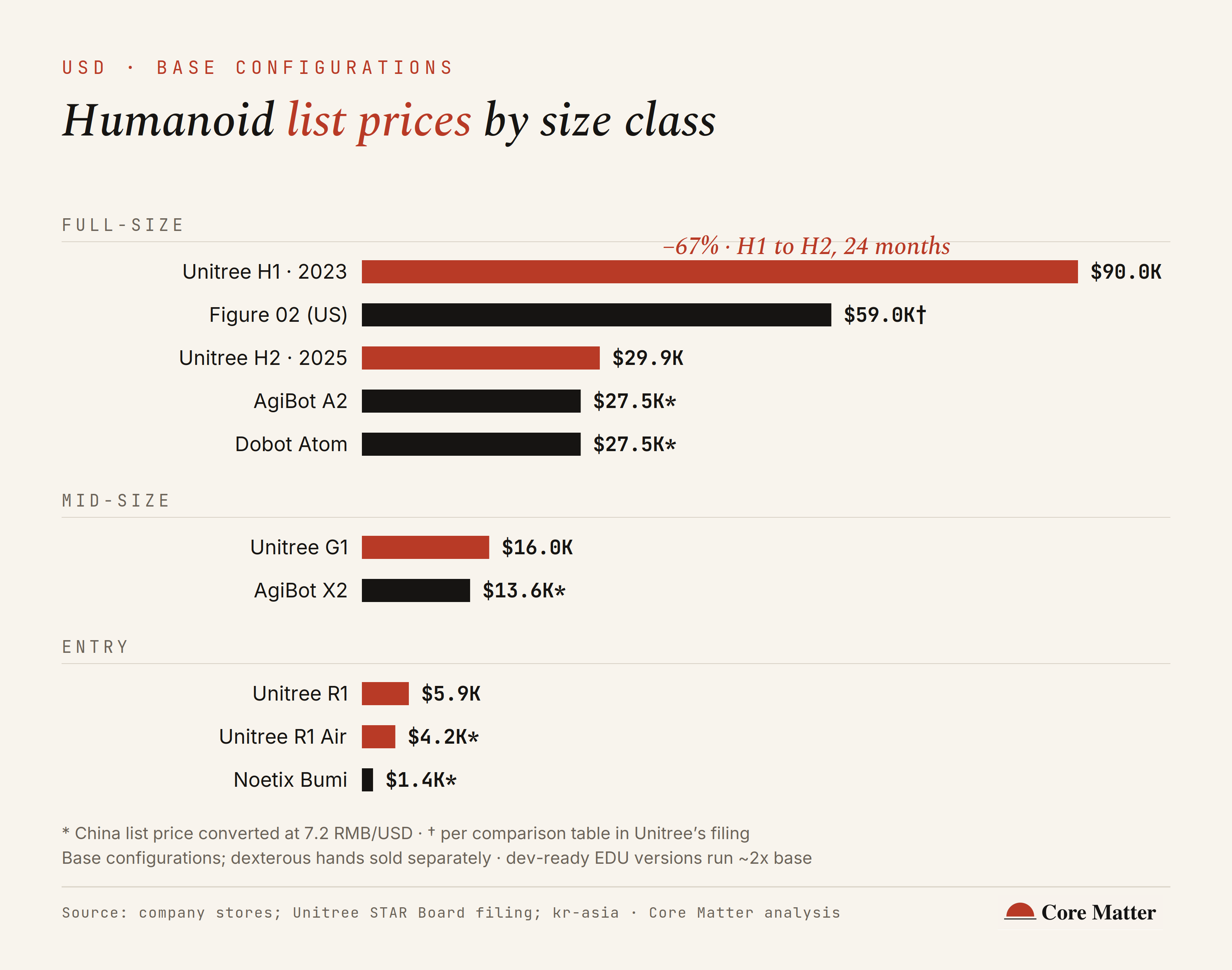

A full-size humanoid body now starts at $29,900. Unitree’s H2, launched October 2025, lists at that price on the company’s international store. Its 2023 predecessor, the H1, still lists at $90,000. This is a 67% price cut in two years. The mid-size G1 lists at ~$16,000 (launched May 2024 at Rmb99K domestic, since cut to Rmb85K). The entry R1 line runs $4,300 to $5,900 (Exhibit 6).

Base prices exclude dexterous hands, sold separately. Unitree pays ~Rmb16K (~$2.2K) per purchased hand. And development-ready configurations run roughly double: the H2 EDU is ~$68,900 through North American distributors versus $29,900 base direct. The body costs $30K, working development platform is $70K. That still sits at a fraction of the field.

The competition is converging on the same floor. Dobot’s Atom and AgiBot’s A2 both list at ~Rmb198K (~$27.5K). AgiBot’s X2 sits at Rmb98K (~$13.6K). Figure 02 lists at ~$59,000 in the comparison table Unitree filed. Boston Dynamics’ Atlas and Tesla’s Optimus are not for sale.

And the floor keeps moving below Unitree: Noetix’s Bumi, limited mobility but a real biped, launched at Rmb9,998, about $1,400.

Unitree describes itself as the sector’s “pricing anchor”: it launches first and lowest, and competitors price relative to it.

But cheaper hardware is not enough to get the robots to do real work. A $16K G1 body is now at a year of fully-burdened wages for one manufacturing worker in the Yangtze River Delta. So on a labor cost basis, the math already works. The 3% problem persists anyway, because the gap is in what the robot can do, not what it costs. We discuss that gap in section 8.

Who makes money today?

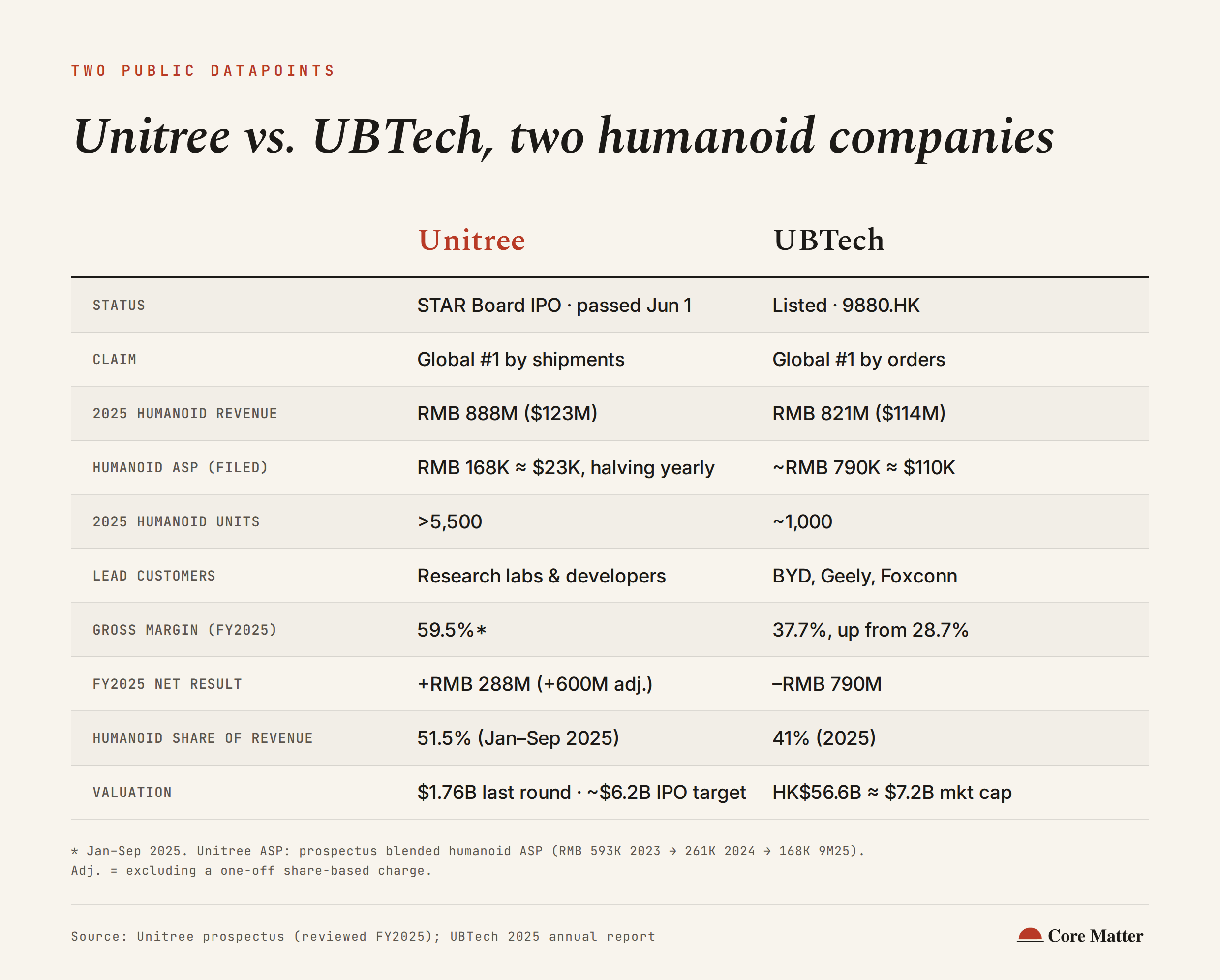

One company in the field discloses a profit, and it is the one selling the cheapest robots (Exhibit 7). Unitree ended FY2025 with Rmb288mn of reported net income, Rmb600mn ($83mn) excluding a one-off share-based charge, on Rmb1.7bn ($237mn) revenue. The profit is company-level. Its mature quadruped line contributes, but the humanoid mix is research-led, low-ASP, high-volume.

That is a company profit, not a humanoid profit. Humanoid gross margin is disclosed, 62.9% for the first nine months, but Unitree does not break out humanoid net, and a research-led mix at a sub-$23K ASP does not make the humanoid line profitable on its own. The mature quadruped business, seven years from research platform to industrial category, is what carries the company into the black.

Every disclosed P&L from a company running the industrial-deployment playbook shows losses. UBTech posted a 2025 net loss of Rmb789.8mn ($110mn), narrowed 32% from Rmb1,159.9mn ($161mn). The loss is not a unit-economics problem: UBTech makes money on each robot, at 37.7% gross margin, and loses it on the Rmb1.3bn operating expenses. The US players disclose nothing; their burn is inferred only from fundraising cadence.

The contrast is about research-led volume versus industrial deployment. UBTech sells industrial-grade Walker S2 robots to BYD, Dongfeng Liuzhou Motor, Geely, and Foxconn at $110K, 1,000 units deployed, the deepest industrial humanoid record anywhere. Unitree sells G1s to researchers at $16K.

Customer overlap is minimal. And unit economics are an order of magnitude apart.

One model is profitable today. The other is subsidizing for deployment and the data that comes with it.

UBTech trades at $7.2bn; ~25X revenue. Unitree, profitable, last raised at $1.76bn, roughly 7X. Applied UBTech’s multiple to Unitree’s FY2025 revenue, the implied value is $6bn+ before any profitability premium.

Unitree passed the SSE listing committee on June 1. Its listing will set the first market-clearing price for a profitable humanoid maker, and test whether profit or deployment is what gets paid for.

Can Unitree win the world and still lose the US?

Aside from deployment metrics, there is a second ceiling, and it is political.

From its current trajectory, Unitree looks like it’s running DJI’s playbook: dominate, scale, become indispensable. Yet, DJI’s dominance triggered Entity List action, and BYD’s global EV lead triggered 100% US tariffs and near-total exclusion from the US market.

If that history is a guide, the pattern for Chinese hardware companies is consistent: dominate everywhere except the US, because dominance is what triggers the US response.

Unitree is now living that pattern on an accelerated timeline.

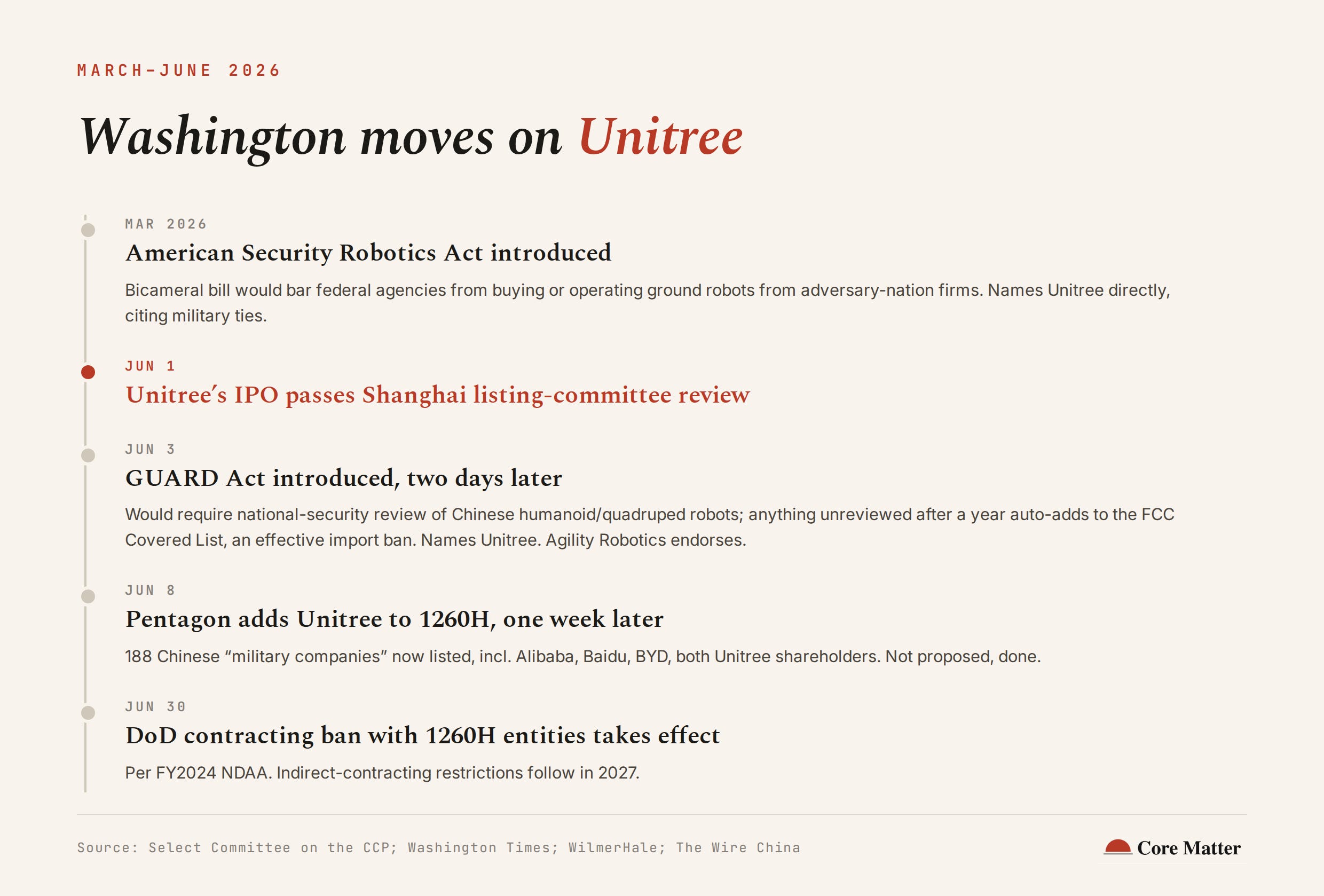

Three actions from Washington in three months show the trend line (Exhibit 8).

In March 2026, a bipartisan, bicameral bill, the American Security Robotics Act, proposed barring federal agencies from buying or operating ground robots from companies in adversary nations. Lawmakers named Unitree directly, citing its ties to the Chinese military.

On June 1, the GUARD Act (Guarding the US Against Adversarial Robotics Dominance Act of 2026), was introduced in the House. It would require a national security review of humanoid and quadruped robots from China. Unreviewed products would be automatically added to the FCC’s Covered List after a year, effectively a US import ban. Its sponsors name Unitree directly. Agility Robotics, a direct US competitor, endorses the bill.

On June 8, the Pentagon added Unitree to its Section 1260H list of Chinese military companies, alongside Alibaba, Baidu and BYD, bringing the list to 188 entities. Unlike the other two, this isn’t proposed, it’s done. The FY2024 NDAA prohibits the Department of Defense from entering or renewing contracts with 1260H-listed entities starting June 30, 2026, with indirect-contracting restrictions following in 2027.

Its competitive strength may be exactly why global dominance isn’t available to Unitree. The better it performs - on cost, on shipment, on the capital markets - the faster Washington moves. “Global domination” and “winning the US market” may simply be two different claims, and as of this month, only one of them is on the table for a Chinese robotics company.

Is “China-body, American-brain” true?

A common belief in robotics is that China builds the body and the US builds the brain. On the open benchmarks built to test it, that has stopped being true. The closed source US embodied models, though, do not compete on these boards at all.

AgiBot has made the broadest public progress. Its AgiBot World dataset holds more than 1M real-robot trajectories across 217 tasks, released end-2024; its Finch unit’s τ0-WM is a 5B world model trained on roughly 27,300 hours, 17,800 of them real-robot teleoperation, open-sourced on GitHub and HuggingFace in May 2026. A companion Finch paper updates VLA models online across deployed fleets, improving them within hours.

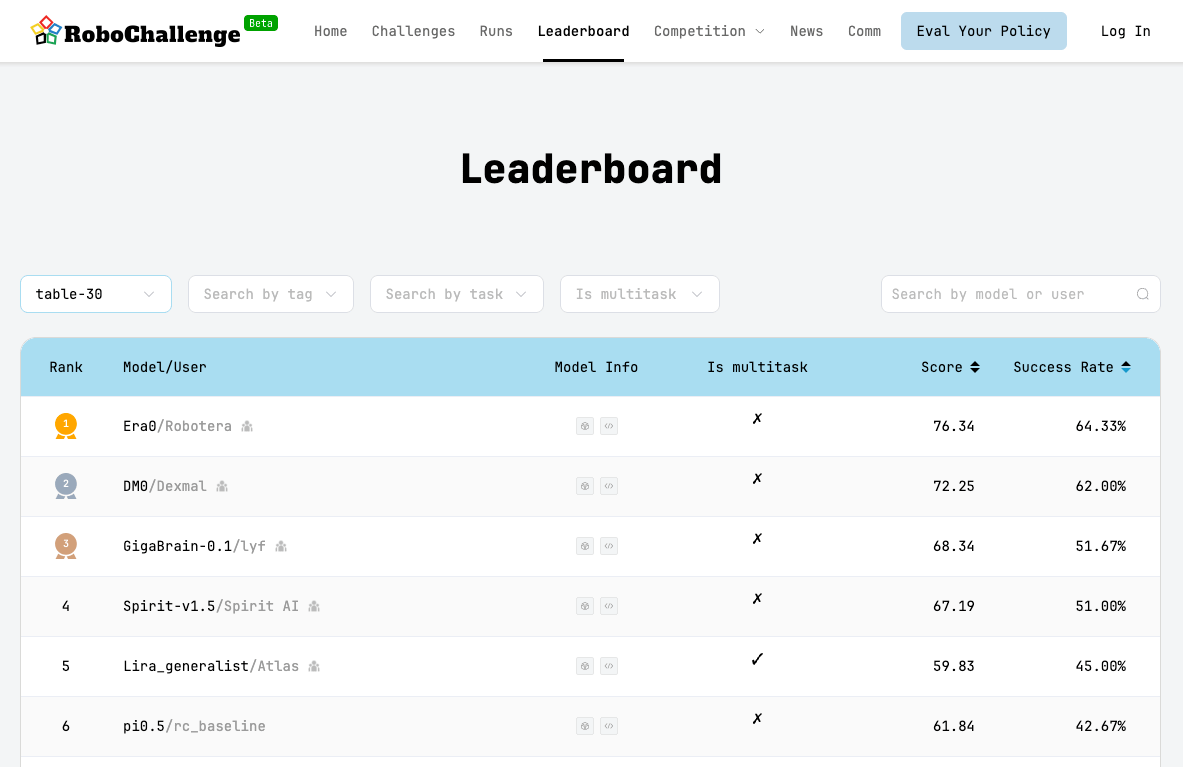

The leaderboard tells the same story (Exhibit 9). Since RoboChallenge launched in October 2025, the live #1 has never been a US lab. Spirit AI‘s open-sourced Spirit v1.5 took it in January 2026; Dexmal’s DM0, also open, took it in February; as of this week Robotera’s Era0 leads, with DM0 second, GigaBrain-0.1, a Wuhan collaboration, third, and Spirit v1.5 fourth. Physical Intelligence’s π-0.5, which the benchmark’s own October paper called remarkably stronger than its rivals, currently ranks sixth.

The pipeline behind the models is the one this report is about. LeJu fed nearly 10,000 hours of multimodal real-robot data into LingBot-VLA, open-sourced as a “universal brain” by Robbyant, an embodied-AI arm of Ant Group, in January 2026. A hardware maker’s deployment data trains a software giant’s model. In February 2026, Unitree posted a video of its UnifoLM model assembling G1 components on Unitree’s own line.

Not every Chinese brain needs a fleet. Galbot released GraspVLA and TrackVLA on 99% synthetic data through NVIDIA’s simulation stack, a sim-first path that skips deployment data, and a reminder that the open Chinese ecosystem still runs on US simulation infrastructure. Robotera says its ERA-42 VLA runs end-to-end in a live logistics warehouse; TARS open-sourced the first large-scale real-world vision-language-tactile-action dataset in December 2025. Astribot, X Square, and Galaxea are a separate deep dive.

The closed frontier models, Gemini Robotics and Helix, do not appear on open benchmarks at all.

On the measurable, open half of the field, “China’s brain is behind” is no longer true. On top of that, the inputs that move these models, fleet data, deployment hours, open ecosystems, iteration speed, are accruing faster on the Chinese side. The tour-guide and entertainment deployments feed data collection, funded by customers rather than by venture capital.

We look at the “brain” scorecard on four axes (Exhibit 10). China leads three: open-benchmark performance, the data flywheel, and open ecosystems. The fourth, the closed US frontier, is unmeasured.

What still stands between humanoids and real work?

Unitree’s risk disclosure names two gates.

The first is embodied-model generalization: data gathered in labs and single scenes does not transfer to oily floors, line changeovers, and unstructured sites. Until it does, every “industrial deployment” is a supervised pilot, and the domain mix in section 2 shows what that means in revenue terms.

The second is dexterous hands: fineness and durability are not yet at industrial grade. The hands are sold separately for a reason, and the company that ships the most humanoids buys some of its hands from suppliers at $2.2K each rather than calling the problem solved.

Mass industrial and home use awaits breakthroughs in both hardware and software.

For signs of industrial adoption, we track renewals and revenue mix shift. When BYD or Foxconn renews a Walker S2 pilot and scales it, or when a research-heavy mix starts tilting toward industry application in the next filing period, the gate is opening.

For mix shift, we particularly pay attention to the share of humanoid revenue that comes from productive industrial work. At Unitree, the company that ships the most, it is 3 to 4% today. That line is the signal to watch in the next few quarters of filings, before any demo, keynote or shipment record.

Key takeaways

The race is real, multi-player, and Chinese, and no winner is set. Unitree and AgiBot each shipped over 5,000. LeJu, UBTech, Galbot etc, are shipping in volume and growing in multiples into 2026. 90 new manufacturers entered the market in 7 months. There is no decided winner. Also, shipment does not equal industrial or commercial deployment. Research and education make up 73.6% of Unitree’s humanoid revenue, and within the 9% labeled “industry,” 50-70% is showroom tours.

How China got here: demand it built, supply it owns. On demand, the Bootstrapping Ladder shows a four-stage progression: research sales pay down production costs, consumer and commercial sales fund volume manufacturing, state procurement funds deployment learning, industrial pilots generate training data.

On supply, owning the components doesn’t just lower costs; it buys speed. An actuator design that takes months to iterate elsewhere can be done the same day in Shenzhen.

China leads the open benchmarks; the US frontier is unmeasured. The “China builds the body, America builds the brain” framing is outdated as of June 2026: every live #1 on RoboChallenge, the leading real-robot benchmark, has been a Chinese open-source model since January 2026. AgiBot, LeJu, and Unitree’s own UnifoLM run open, fleet-fed models at a pace and openness the closed US labs aren’t matching. What the open boards cannot see, Tesla, Figure, Gemini Robotics, Helix, stays unmeasured. Fleet data, deployment hours, and iteration speed are compounding fastest in Shenzhen and Hangzhou.

The price floor fell two-thirds in two years, before the market opened. A full-size humanoid body now lists at $29,900 against $90,000 for its own 2023 predecessor; a working biped starts near $4,300; development-ready configurations run roughly 2X base. The mechanism is filed: 14 to 18% outsourced content and self-built actuators. Unitree’s IPO, past the listing committee as of June 1, will set the first market-clearing price for a profitable humanoid maker. Watch it, and watch renewals, not demos.

The policy ceiling arrived before the IPO did. The DJI and BYD precedents suggest the pattern: Chinese hardware champions dominate everywhere except the US, because dominance is what triggers the US response. Unitree’s cost and integration advantages are real, real enough that Washington is already acting on them. “Global domination” and “winning the US market” may be two different outcomes, and right now only one is available to a Chinese robotics company.

Watchlist

Unitree’s STAR Board IPO pricing (passed the listing committee June 1; registration pending). The category’s first market-clearing price for a profitable maker.

AgiBot’s reported HK IPO plan: whether it separates humanoid revenue from wheeled-form and data-collection revenue, and what its gross margin shows.

EngineAI’s IPO prospectus: filed confidentially on June 12 for Hong Kong IPO.

UBTech’s humanoid mix crossing 50%, and whether the BYD/Geely/Foxconn Walker S2 pilots convert to repeat orders.

RoboChallenge #1: still uncontested by any US lab as of June 2026.

The next Unitree filing period’s domain mix: any shift from research toward industry application is the earliest hard signal that humanoids are starting to do productive work.

This is the first in a series of deep dives reading Physical AI markets through primary filings: humanoids, service and industrial robotics, and the unit economics and supply chains underneath them.

About Core Matter Labs

Core Matter Labs is a Physical AI research and analysis practice covering the founders, researchers, and operators building the intelligence layer for the physical world. Research is built on primary filings, original reporting, and ground-level access to the global hardware supply chain.

www.corematterlabs.co | Copyright © 2026 Core Matter Labs | All rights reserved.